Speak To Our Experts

Get the Right Coverage at the Best Price

“Richey Insurance Agency works for you, not just one insurance agency!”

Trustindex verifies that the original source of the review is Google. My contact was Chan. He was very helpful and accommodating and provided excellent service.Posted on GoogleTrustindex verifies that the original source of the review is Google. Very good insuranes very happy with this services thank you.Posted on GoogleTrustindex verifies that the original source of the review is Google. Muy buen servicio y muy buena compañía de segurosPosted on GoogleTrustindex verifies that the original source of the review is Google. Used for commercial insurance, quick to respond and get us what we need.Posted on GoogleTrustindex verifies that the original source of the review is Google. Richey Insurance handles my homeowners policy and they’ve been excellent to work with. Anytime I have a question or need something taken care of, they get back to me right away with clear answers. Highly recommend them if you want an agency that actually responds and gets things done.Posted on GoogleTrustindex verifies that the original source of the review is Google. They are great, always communicative and proactive!Posted on GoogleTrustindex verifies that the original source of the review is Google. so far I have been told the truth Insurance price is what was quoted iprace honestly Paul straight up so far

It only takes a few moments to complete the form, request a quote now!

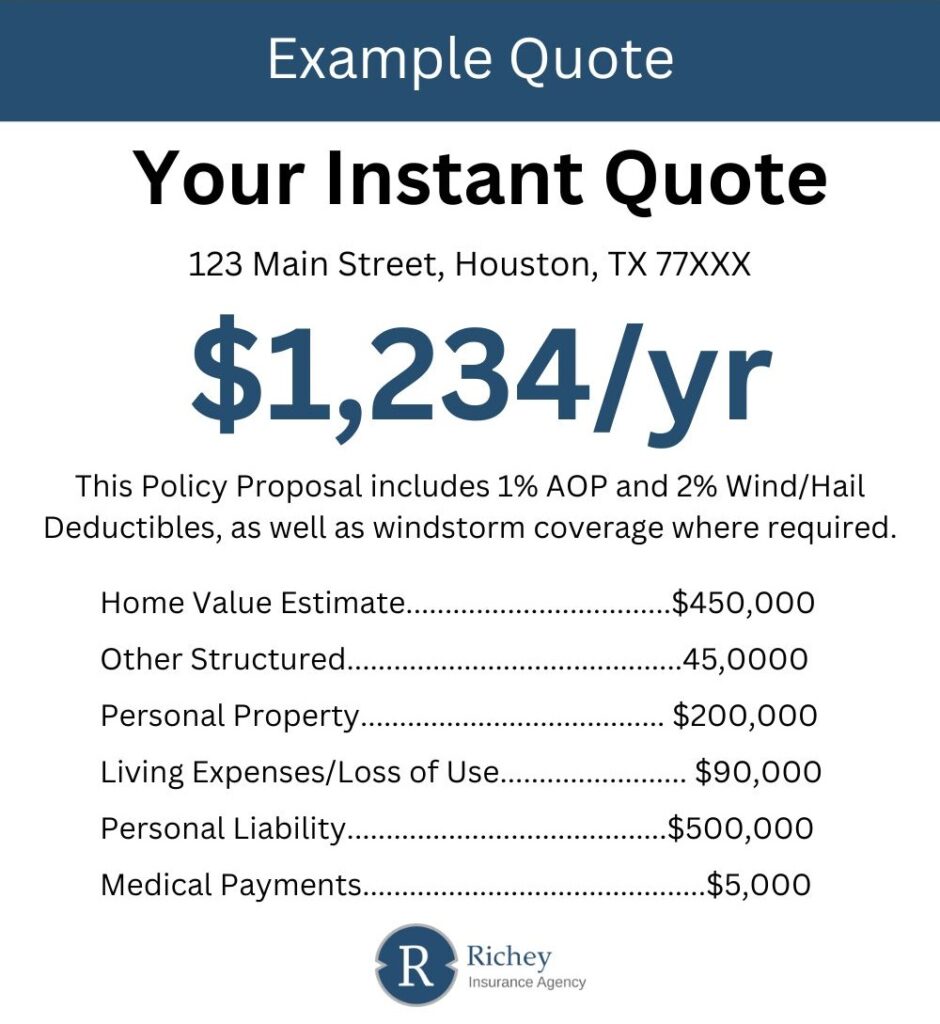

The image provided is a representation of what your quote will look like.

A standard homeowners insurance policy protects against a range of risks. Here’s what it covers:

Home insurance provides solid protection, but certain risks call for specialized coverage options.

Yes. A homeowners policy includes appliances under personal property coverage. If a named peril, like fire or theft, damages them, the policy helps cover repair or replacement costs.

Rates have climbed over the past decade, with some estimates showing a 60% increase. Inflation, rising construction costs, and frequent disasters contribute to this trend. Locking in a policy now can help secure a stable rate.

Yes, fire damage is covered. Insurance helps repair or rebuild the home, replace personal belongings, and pay for temporary living costs while repairs are made. Fire claims are among the most expensive, so having coverage matters.

Policies must cover at least 80% of a home’s replacement cost to receive full reimbursement on claims. Falling below this percentage may result in reduced payouts, meaning out-of-pocket expenses for repairs.

Keeping costs in check doesn’t require sacrificing coverage. A few strategies that may help:

Yes. In most states, insurers use a credit-based insurance score to help determine premiums. A lower credit score—typically below 630—may result in higher rates. Improving credit history by paying bills on time and reducing outstanding debt can lead to better insurance pricing.

Request a free quote using our convenient online form

Prefer to talk to a representative? Our agents are more than happy to help you.

You are welcome to visit our office. We are open Monday - Friday (8 am - 5 pm)

Compare auto insurance rates from multiple carriers in Rosharon, Texas.