Speak To Our Experts

Compare 100+ Home Insurance Carriers with One Local Agency

“Richey Insurance Agency works for you, not just one insurance agency!”

Trustindex verifies that the original source of the review is Google. My contact was Chan. He was very helpful and accommodating and provided excellent service.Posted on GoogleTrustindex verifies that the original source of the review is Google. Very good insuranes very happy with this services thank you.Posted on GoogleTrustindex verifies that the original source of the review is Google. Muy buen servicio y muy buena compañía de segurosPosted on GoogleTrustindex verifies that the original source of the review is Google. Used for commercial insurance, quick to respond and get us what we need.Posted on GoogleTrustindex verifies that the original source of the review is Google. Richey Insurance handles my homeowners policy and they’ve been excellent to work with. Anytime I have a question or need something taken care of, they get back to me right away with clear answers. Highly recommend them if you want an agency that actually responds and gets things done.Posted on GoogleTrustindex verifies that the original source of the review is Google. They are great, always communicative and proactive!Posted on GoogleTrustindex verifies that the original source of the review is Google. so far I have been told the truth Insurance price is what was quoted iprace honestly Paul straight up so far

It only takes a few moments to complete the form, request a quote now!

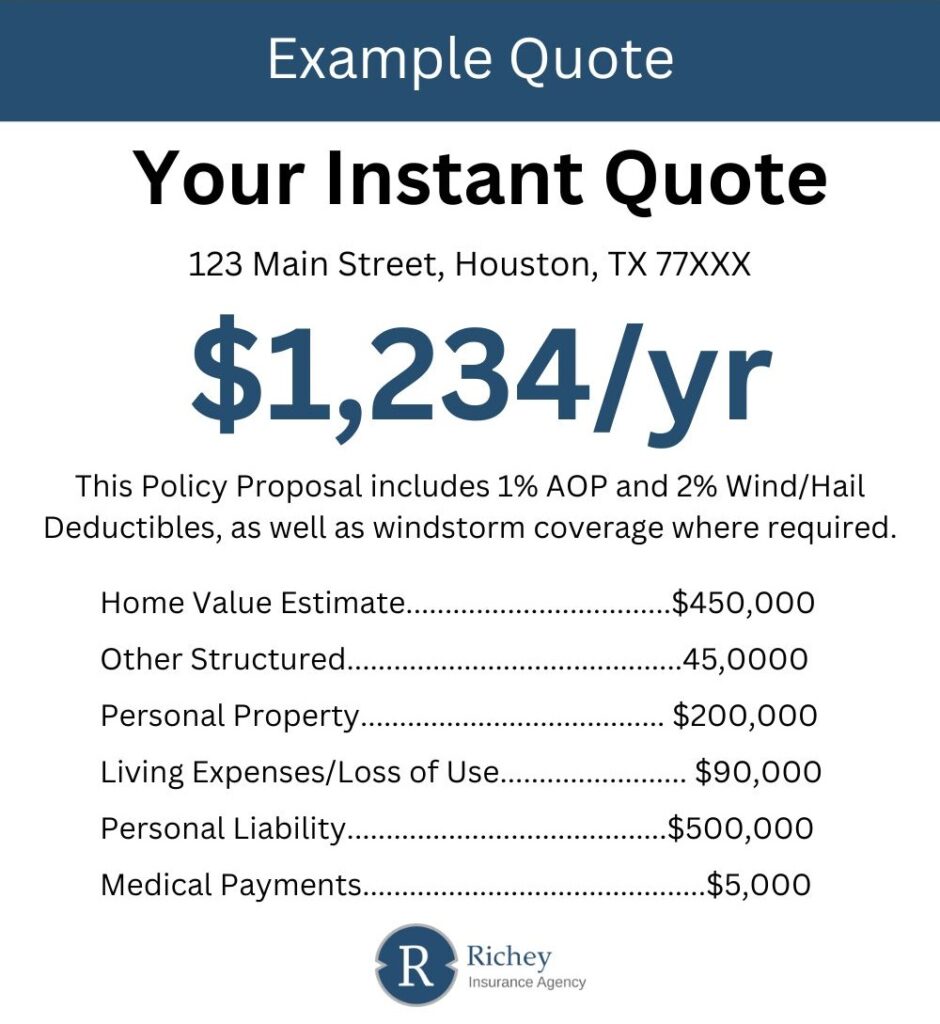

The image provided is a representation of what your quote will look like.

Lubbock may not see much snow, but its weather patterns create a steady stream of risks. In the spring and summer, hailstorms roll across the plains, often leaving behind dents, cracks, and shattered windows. Strong winds are part of life here, and in the right conditions, they can bring down fences, siding, and even roofs. Fires, too, remain a threat, especially during long dry spells in the hotter months.

Every homeowner in Lubbock should consider how their policy handles these risks. Not all coverages are built the same, so it’s worth taking a closer look at how hail, windstorm, and fire protection show up in your current policy or how they might be added if needed.

Yes, most carriers apply the 80% rule. This rule affects how much you receive if you file a claim for a partial loss. For example, if your ranch-style home in the Bowie neighborhood is worth $300,000, you’ll typically need at least $240,000 in coverage to avoid a reduced payout.

It’s a good idea to revisit that number each year, especially after a home remodel or during sharp changes in local property values. An updated replacement estimate helps keep your coverage aligned with your home’s real-world rebuild costs.

Bundling policies is a common way to reduce your insurance bill. Home and auto are the most popular combination, and in many cases, it results in savings of up to 25%. But that’s not the only option.

You might combine home coverage with motorcycle, boat, RV, or even second property insurance. Adding a monitored alarm system or storm shutters may unlock additional discounts. Each insurance carrier is a little different, so working with an independent agency helps match you with the bundle and features that benefit you most.

Yes. Rates have been climbing year over year, and Lubbock is no exception. The increase is tied to the growing number of severe weather events across Texas and beyond. More claims mean higher costs for insurers, which eventually show up in the form of higher premiums for policyholders.

Locking in the right coverage sooner rather than later can help avoid steeper costs in the future.

That depends on what caused the damage. If a covered event like wind or lightning brings a tree down onto your home or fence, your policy may respond. But if the fall was caused by a slow-developing issue like rot or poor maintenance, coverage might be limited.

In some cases, tree damage affects someone else’s property. If a tree from your yard lands on a neighbor’s roof, their policy will likely handle the claim. Still, liability coverage can come into play if you’re found responsible.

It’s worth reviewing how your policy handles different damage scenarios, especially in older neighborhoods where tree growth and property lines often overlap.

Premiums reflect the cost to repair or replace homes, and Lubbock’s claims history plays a role. Hailstorms and wind events are frequent enough to raise risk levels for insurers. Labor and material costs have also gone up, which raises the price of rebuilding after a loss.

Carriers have adjusted their pricing models in response. The result is higher rates across much of Texas, especially in areas with a history of weather-related claims.

Request a free quote using our convenient online form

Prefer to talk to a representative? Our agents are more than happy to help you.

You are welcome to visit our office. We are open Monday - Friday (8 am - 5 pm)

Compare auto insurance rates from multiple carriers in Lubbock, Texas.