Speak To Our Experts

Custom Coverage Matched from 100+ Trusted Carriers

“Richey Insurance Agency works for you, not just one insurance agency!”

Trustindex verifies that the original source of the review is Google. Harold has been such a great resource! He has answered all of my questions and helped ensure that I get the best insurance rate.Posted onTrustindex verifies that the original source of the review is Google. Everyone listen to my questions and worked to get me what I wanted.Posted onTrustindex verifies that the original source of the review is Google. I called today and spoke with Jeesril to confirm information about my automobile coverage. He was very professional, knowledgeable and helpful. He explained to me why the company name had changed and when my next bank draft would be due. I feel very comfortable with the interaction I had with him today and would recommend Richey Insurance Agency to anyone in need of insurance.Posted onTrustindex verifies that the original source of the review is Google. I appreciate the assistance provided by Wincy @Richey Insurance in setting up my auto and home renewals. What draws me to recommend him for your needs is his dedication to go above and beyond in finding the best premiums for your needs without compromising coverage.Posted onTrustindex verifies that the original source of the review is Google. I’ve talked with Darren and Radali. Both are amazing, they listen and find the best insurance policy that fits you… 100% recommended!

It only takes a few moments to complete the form, request a quote now!

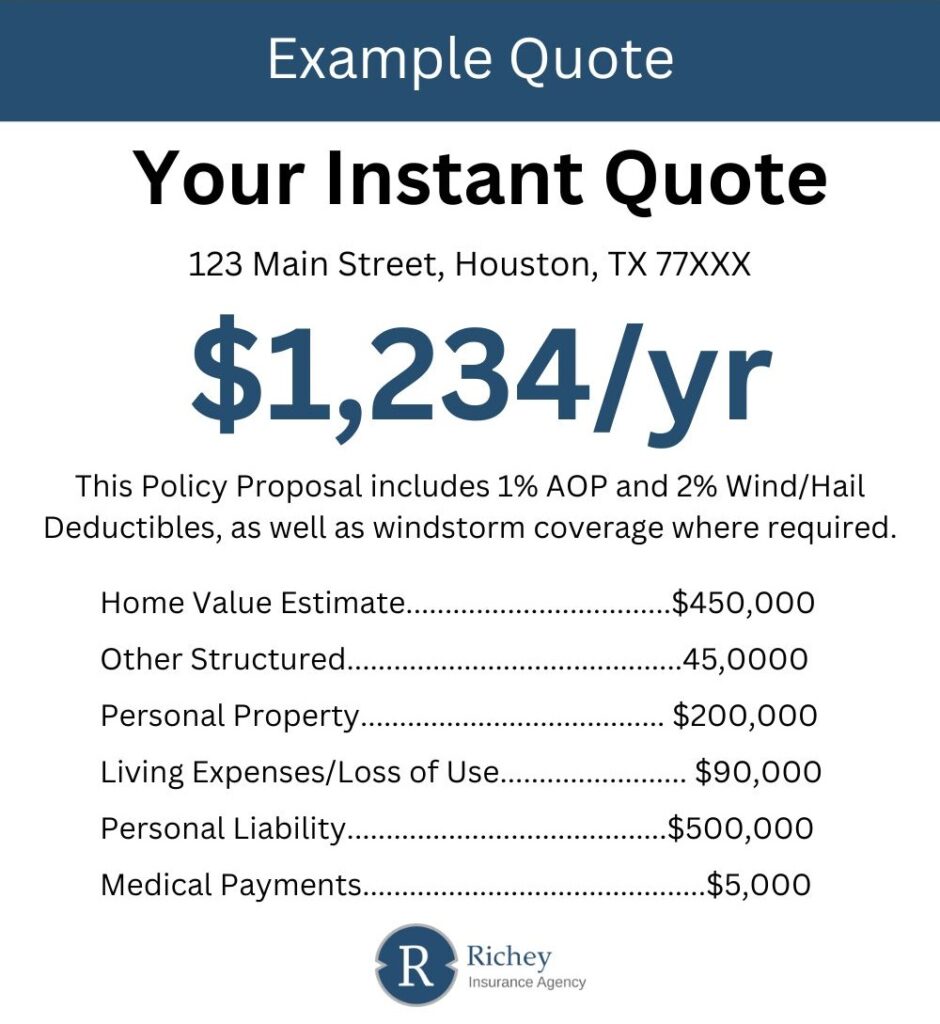

The image provided is a representation of what your quote will look like.

Rates in Hockley aren’t one-size-fits-all. Your premium depends on a mix of location-based risks, home details, and policy choices. Here’s what carriers typically consider:

Many homeowners in Hockley choose extra protection for:

Yes, as long as the damage came from a covered event such as a storm, wind, or lightning, your policy should help pay for repairs.

Yes. If a fire starts from a covered cause, like lightning or an accident, your policy will help pay for damage and temporary housing if needed.

Jewelry is generally covered for specific events like theft or fire, up to a set limit. For higher-value pieces, you may want to schedule them separately in your policy.

Yes. Going claim-free for consecutive years can lead to a lower premium. Many insurers reward a clean claims history with incremental savings over time.

Request a free quote using our convenient online form

Prefer to talk to a representative? Our agents are more than happy to help you.

You are welcome to visit our office. We are open Monday - Friday (8 am - 5 pm)