Speak To Our Experts

Quality Coverage Options Matched to Your Needs from 100+ Trusted Carriers

“Richey Insurance Agency works for you, not just one insurance agency!”

Trustindex verifies that the original source of the review is Google. We have worked with this insurance company for over 10 years. They have consistently provided reliable coverage, responsive service, and clear guidance when we’ve needed it most. We appreciate the long-term relationship and professionalism.Posted onTrustindex verifies that the original source of the review is Google. Mr. Paul was very helpful in meeting my insurance needs. Also their price was less than what was quoted by other agentsPosted onTrustindex verifies that the original source of the review is Google. Respectful and courteous! Meets all demands and questions. Very cooperative. Paul is very easy to work with. Thank you guys!Posted onTrustindex verifies that the original source of the review is Google. Paul was very kind and very helpfulPosted onTrustindex verifies that the original source of the review is Google. Richey Insurance is the best!!!Posted onTrustindex verifies that the original source of the review is Google. Great service

It only takes a few moments to complete the form, request a quote now!

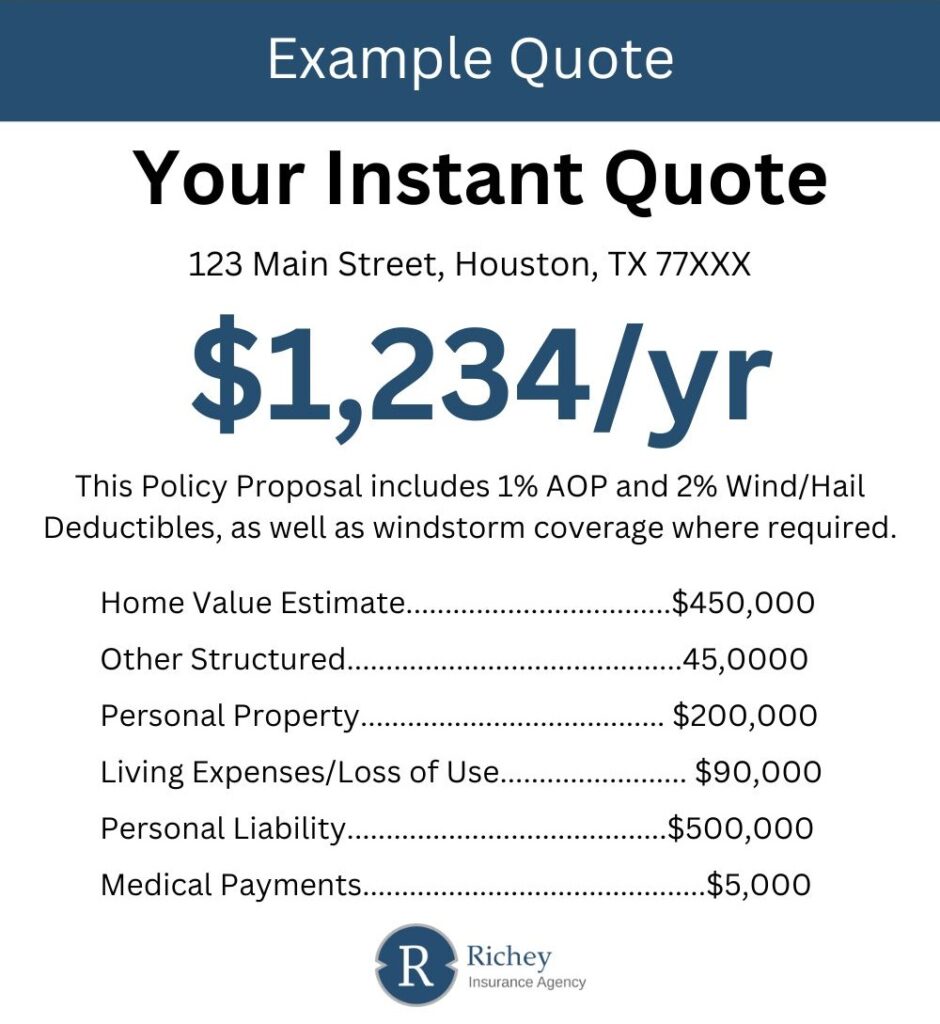

The image provided is a representation of what your quote will look like.

A typical homeowners insurance policy is built to help repair, replace, or recover from damage or loss. While each policy may vary, most include a familiar group of protections:

Optional endorsements like flood or water backup coverage are available if you need added protection.

Yes. Most insurance companies check your credit-based insurance score when pricing a policy. Strong payment history often translates to lower premiums. Homeowners with poor credit may see rates rise significantly sometimes over $1,000 more annually.

It does. Homes with wood framing tend to cost more to insure due to their fire and storm vulnerability. Brick, stucco, and stone homes may come with lower premiums thanks to better durability, though these materials often cost more to replace after damage.

Often, yes. Older properties may require specialized materials and craftsmanship, which increases rebuilding costs. Plaster walls, wood floors, and detailed trim can drive rates up. However, age alone cannot be used as the sole reason to deny coverage.

Consider installing safety upgrades like a monitored alarm system, reinforcing your roof, or replacing aging wiring or plumbing. Raising your deductible, bundling with auto insurance, and shopping carriers can help reduce costs too.

$100,000 is usually the minimum, but many homeowners choose limits between $300,000 and $500,000. This helps protect your assets in case of a serious accident or legal claim.

Request a free quote using our convenient online form

Prefer to talk to a representative? Our agents are more than happy to help you.

You are welcome to visit our office. We are open Monday - Friday (8 am - 5 pm)