Speak To Our Experts

One Local Agency. Over 100 Home Insurance Options

“Richey Insurance Agency works for you, not just one insurance agency!”

Trustindex verifies that the original source of the review is Google. My contact was Chan. He was very helpful and accommodating and provided excellent service.Posted on GoogleTrustindex verifies that the original source of the review is Google. Very good insuranes very happy with this services thank you.Posted on GoogleTrustindex verifies that the original source of the review is Google. Muy buen servicio y muy buena compañía de segurosPosted on GoogleTrustindex verifies that the original source of the review is Google. Used for commercial insurance, quick to respond and get us what we need.Posted on GoogleTrustindex verifies that the original source of the review is Google. Richey Insurance handles my homeowners policy and they’ve been excellent to work with. Anytime I have a question or need something taken care of, they get back to me right away with clear answers. Highly recommend them if you want an agency that actually responds and gets things done.Posted on GoogleTrustindex verifies that the original source of the review is Google. They are great, always communicative and proactive!Posted on GoogleTrustindex verifies that the original source of the review is Google. so far I have been told the truth Insurance price is what was quoted iprace honestly Paul straight up so far

It only takes a few moments to complete the form, request a quote now!

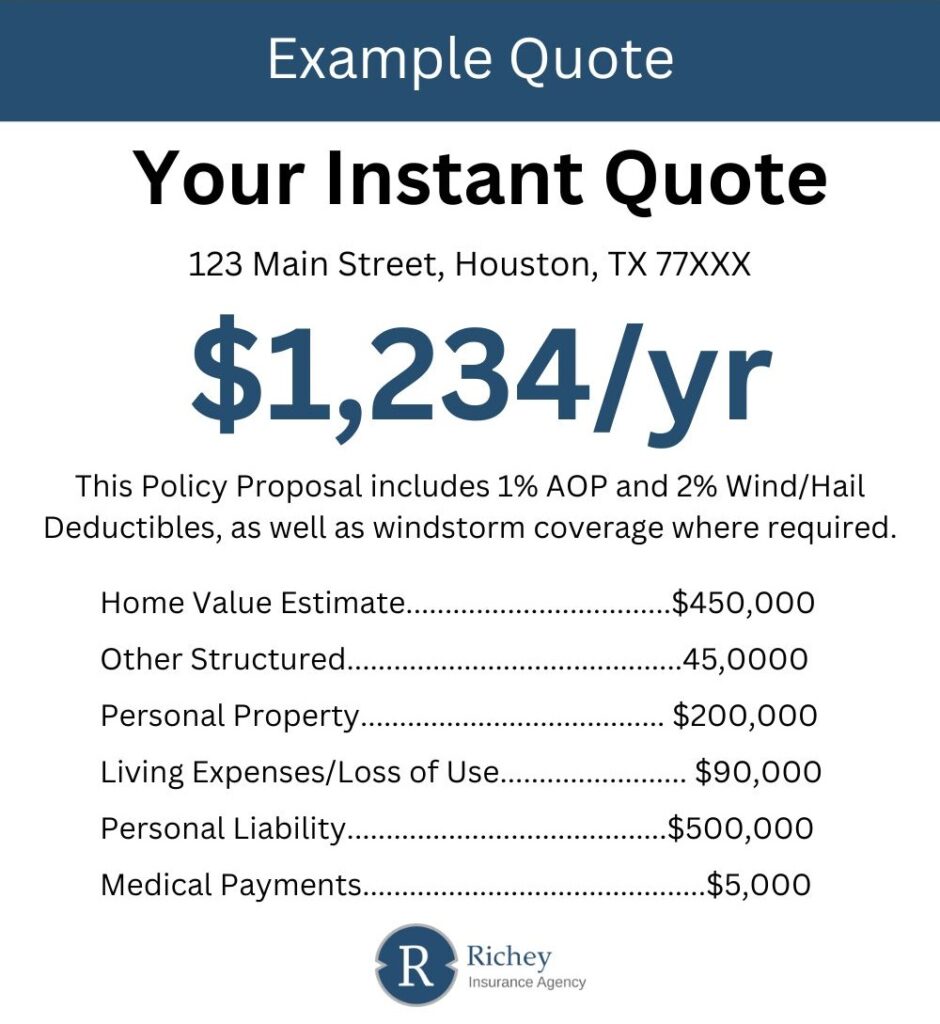

The image provided is a representation of what your quote will look like.

Home insurance pricing isn’t fixed. Rates can vary house to house, even on the same block. Factors like construction type, claims history, and local risk play a big role in shaping your premium.

Here’s how Liberty compares:

Paying far less than the city average? You might be carrying limited coverage and paying more? You may be overinsured or paying too much for what you need.

Carriers use several factors to set pricing. Some are personal, others are environmental. Here are some key ones:

Rates aren’t set in stone. Comparing quotes across multiple carriers can help you land the best value, without cutting corners on protection.

There’s no single fix, but these adjustments could lead to a more competitive quote:

A home insurance quote is an estimate of the premium based on your property details, risk factors, and selected coverages. It gives you a preview of what a policy may cost before you commit.

Yes. Carriers still offer coverage if you have low credit, though your rate may be higher. A low score signals more risk statistically, which can affect pricing but it doesn’t block you from qualifying.

Yes. Most homeowners policies include fire damage unless specifically excluded. If fire makes your home unlivable, your policy may also cover temporary living expenses while repairs are made.

In many cases, yes. Submitting a claim especially for larger losses can lead to a rate increase at renewal. That’s why many homeowners choose to pay for smaller repairs out of pocket.

Request a free quote using our convenient online form

Prefer to talk to a representative? Our agents are more than happy to help you.

You are welcome to visit our office. We are open Monday - Friday (8 am - 5 pm)

Compare auto insurance rates from multiple carriers in Liberty, Texas.