Speak To Our Experts

Affordable Coverage That Works as Hard as You Do

“Richey Insurance Agency works for you, not just one insurance agency!”

Trustindex verifies that the original source of the review is Google. My contact was Chan. He was very helpful and accommodating and provided excellent service.Posted on GoogleTrustindex verifies that the original source of the review is Google. Very good insuranes very happy with this services thank you.Posted on GoogleTrustindex verifies that the original source of the review is Google. Muy buen servicio y muy buena compañía de segurosPosted on GoogleTrustindex verifies that the original source of the review is Google. Used for commercial insurance, quick to respond and get us what we need.Posted on GoogleTrustindex verifies that the original source of the review is Google. Richey Insurance handles my homeowners policy and they’ve been excellent to work with. Anytime I have a question or need something taken care of, they get back to me right away with clear answers. Highly recommend them if you want an agency that actually responds and gets things done.Posted on GoogleTrustindex verifies that the original source of the review is Google. They are great, always communicative and proactive!Posted on GoogleTrustindex verifies that the original source of the review is Google. so far I have been told the truth Insurance price is what was quoted iprace honestly Paul straight up so far

It only takes a few moments to complete the form, request a quote now!

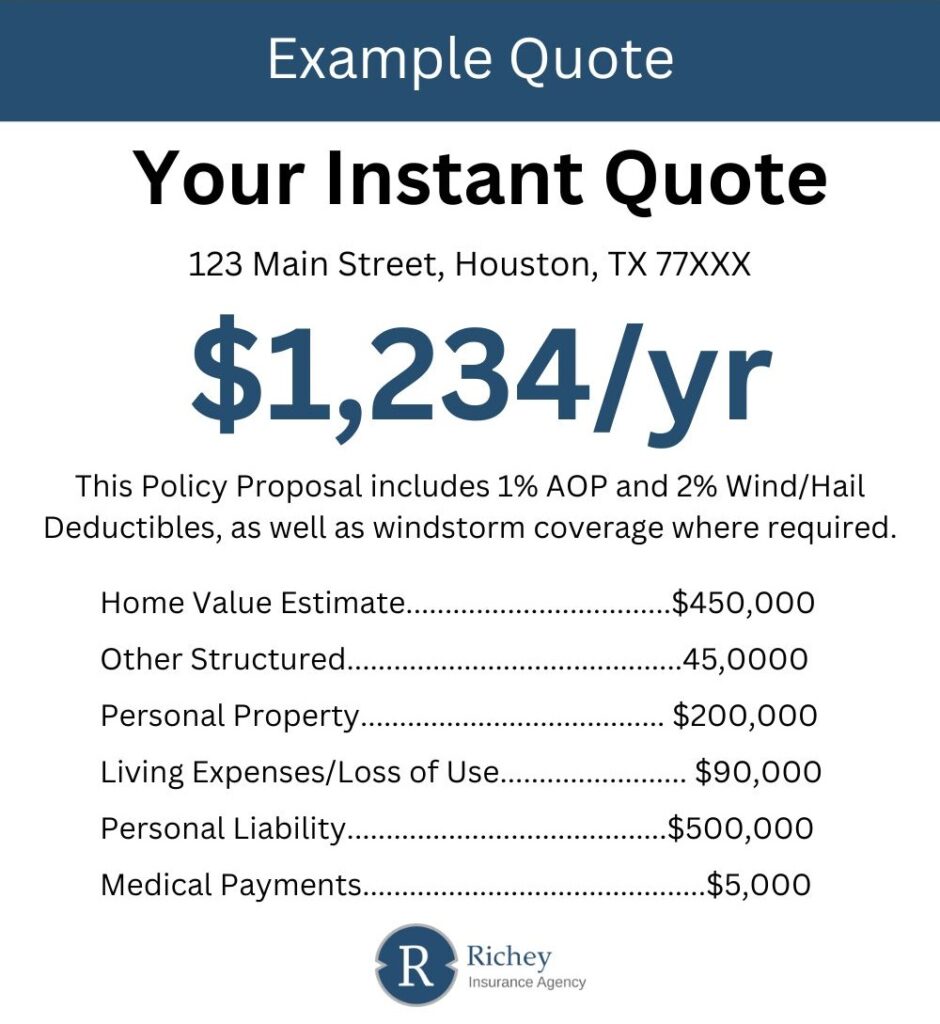

The image provided is a representation of what your quote will look like.

Insurers weigh multiple details before giving a quote. Each one reflects how much risk your home carries—and how much it’ll cost to protect.

| Factor | Why It Matters |

|---|---|

| Home Age & Build Type | Older homes or unique structures may need pricier materials or repairs. |

| Location & Proximity to Coast | Areas prone to storms or flooding influence higher rates. |

| Roof Shape & Materials | Certain roof types are more storm-resistant than others. |

| Security Features | Alarms and cameras can lower your premium. |

| Pets & Play Equipment | Pools, trampolines, and certain dog breeds might raise liability concerns. |

No two homes—or homeowners—are alike. That’s why Richey Insurance Agency compares dozens of carriers to find the rate that fits your situation.

Standard policies cover the basics—but Texas weather calls for more than basic protection. Here are two smart additions to consider:

These options strengthen your safety net and provide a clearer path to recovery after extreme weather hits.

Even the broadest plans leave out some specific events or losses. These aren’t usually covered unless you specifically request extra protection:

A simple way to avoid surprises? Ask your agent what gaps exist and how to fill them before damage occurs.

Home insurance covers costs related to damage, destruction, or liability tied to your home. Most policies bundle six coverage types:

Yes—if the damage came from a covered event like hail, wind, or fire. But if the roof simply wore out over time, repairs fall on the homeowner. Insurance won’t cover deterioration from age or neglect.

You can. Richey Insurance Agency offers online quote tools to get you started quickly. Still, working directly with one of our agents gives you clarity on coverage options—and might uncover discounts you didn’t expect.

Dwelling coverage. It protects the structure of your house and serves as the base of your policy. Most policies calculate other coverages (like personal property or other structures) as a percentage of your dwelling amount.

In most cases, damage from pests like rodents, insects, or termites is excluded. Routine pest control is considered a maintenance task, not an insurable loss. That said, if an undetected infestation causes serious structural failure, you may have a case—just don’t expect reimbursement for minor damage or exterminator fees.

Request a free quote using our convenient online form

Prefer to talk to a representative? Our agents are more than happy to help you.

You are welcome to visit our office. We are open Monday - Friday (8 am - 5 pm)

Compare auto insurance rates from multiple carriers in Kyle, Texas.